Want to Get Rich? Start Collecting Parking Tickets — It’s Not as Crazy as It Sounds

Want to Get Rich? Start Collecting Parking Tickets — It’s Not as Crazy as It Sounds

Why paying parking fines might be a smart move, how compounding in S&P 500 and Bitcoin works, and why even a tiny BTC allocation can boost your returns. Plus, the quickest ways to get rid of debt.

Reading time: 6 minutes

Charts 2-Pack

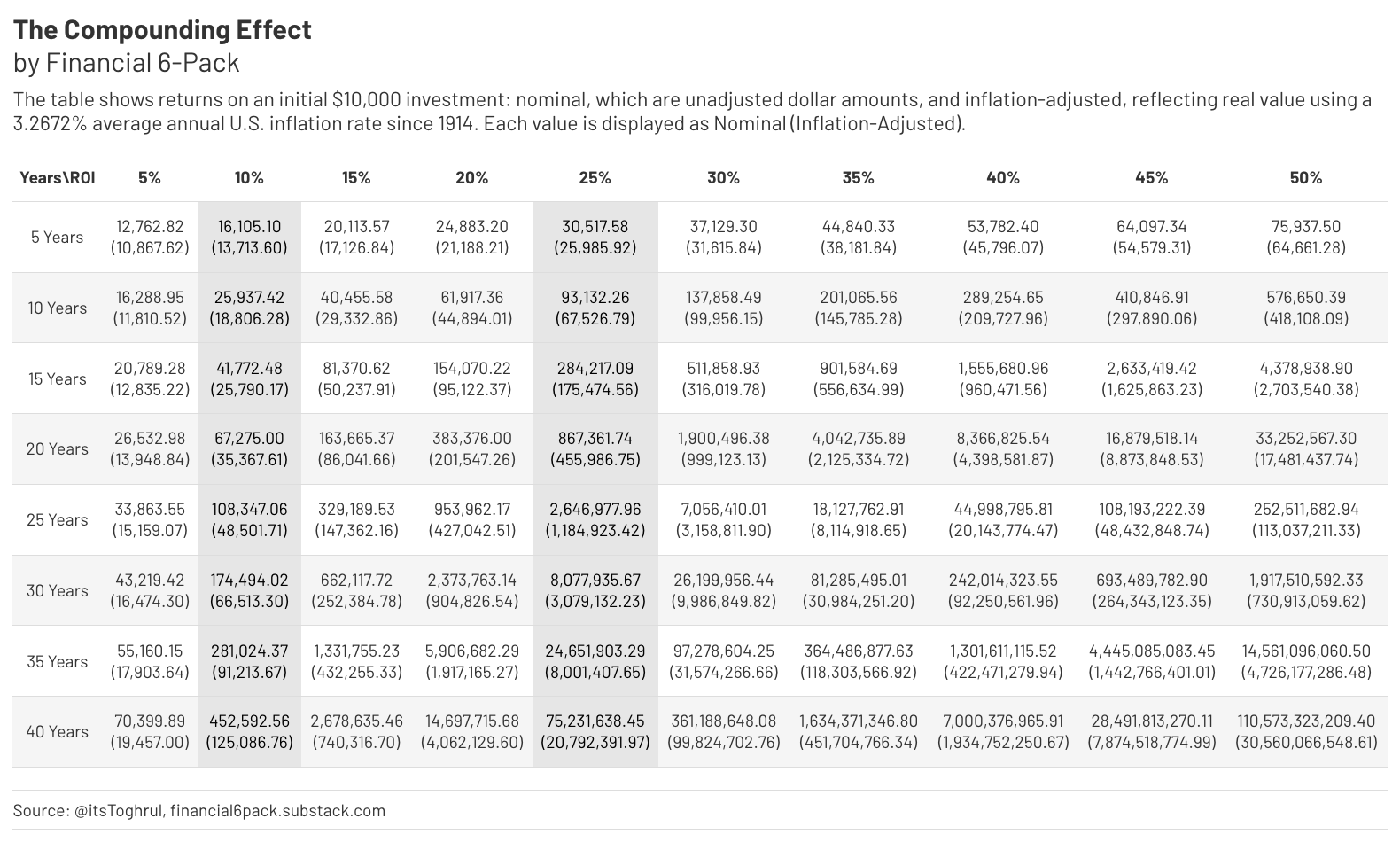

Compounding Turns Small Investments into Big Gains

I want to present two scenarios. One involves investing in the S&P 500, and the other in Bitcoin.

Since its inception in 1957, the S&P 500 has returned an average of 10% per year, taking into account all market highs, lows, and economic crises.

Bitcoin, on the other hand, has had a compound annual growth rate (CAGR) of about 100% since 2011. However, that explosive growth rate has slowed. For example, since 2017, its growth has averaged around 46.59%.

While Bitcoin is experiencing rapid global adoption, we can expect future growth rates to oscillate between 45% and 60% conservatively. To be more cautious, let's assume a 25% annual return for Bitcoin going forward.

Now, take a look at the table, specifically the columns showing 10% and 25% returns. This is why compounding is amazing.

Let's say you can wait 10 years.

If you invest $10,000 today in VOO (S&P 500), you'd have $25,937.42 after a decade—a solid 2.6x return. But if you had chosen Bitcoin instead, your $10,000 could grow to $93,132.26, a staggering 9.31x return.

Consider the long-term perspective.

Maybe you're in your early 20s, or perhaps you're a parent investing in your newborn child. If you invest $10,000 from birth, by the time they turn 20 (or you turn 40), that investment could grow to $67,275 in the S&P 500 or an astounding $867,361.74 if placed in Bitcoin.

The difference compounding makes is enormous, and even a 5% change in the rate of return can lead to drastically different outcomes.

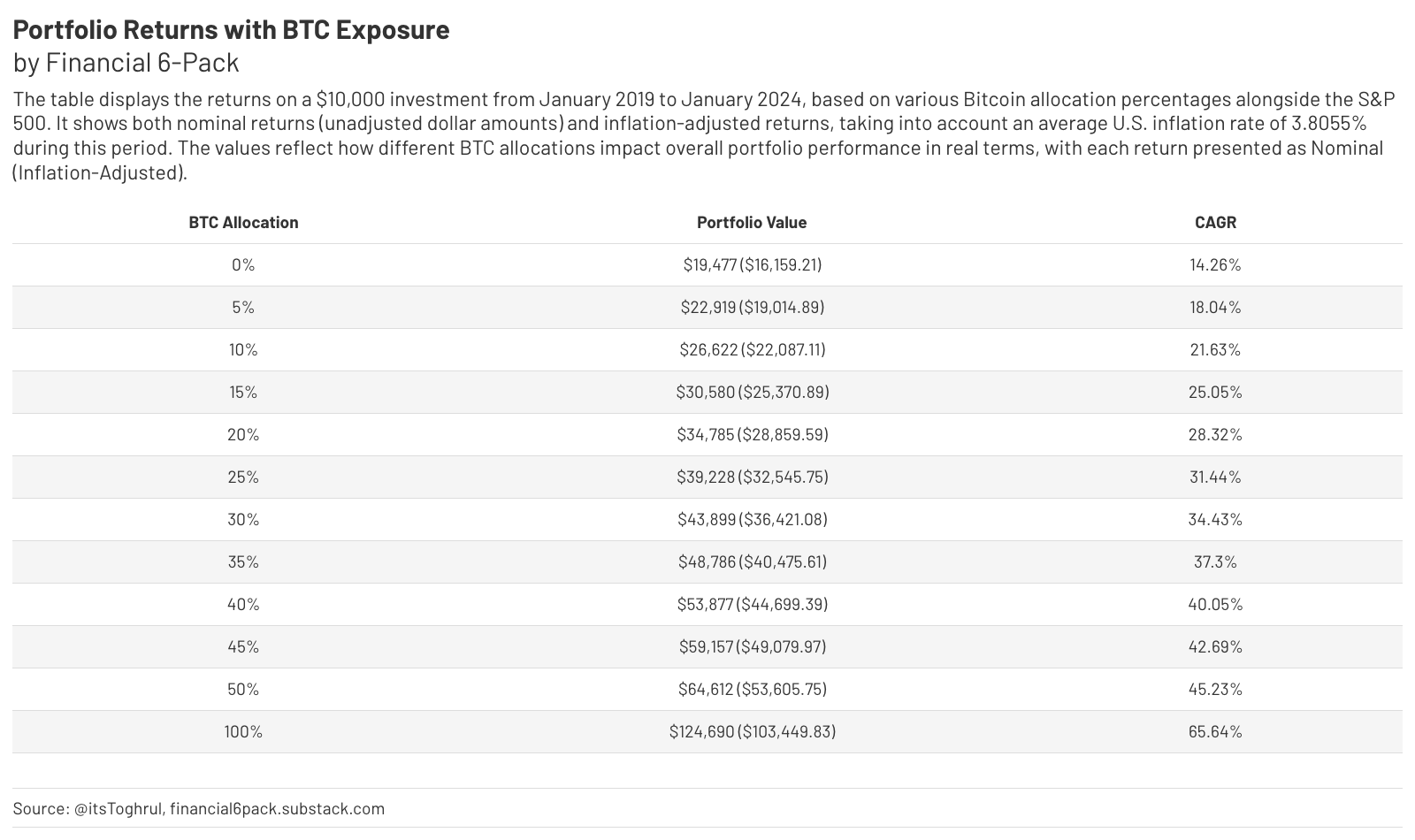

Small Bitcoin Allocation, Big Rewards

Let's say you don't believe in Bitcoin at all. You want to stick with low-risk investments like the S&P 500 because it feels safer. Well, the second table I'm showing might surprise you.

Over the last 5 years, if you had allocated just 10% of your portfolio to Bitcoin and kept 90% in the S&P 500, you would have increased your returns by 36.68% compared to investing 100% in the S&P 500 alone.

If you took it a step further and allocated 50% to Bitcoin and 50% to the S&P 500, your portfolio would have experienced a 3.33x increase in returns than if you'd stayed 100% in the S&P 500.

The beauty of this strategy is that you're not going all-in on Bitcoin; instead, you're simply adding enough to supercharge your returns while still leaning on the reliable performance of the S&P 500. That balance between traditional and alternative assets can enhance your portfolio's growth without exposing you to the full risk of Bitcoin's volatility.

Knowledge 2-Pack

The Secret to Becoming Debt-Free Faster

Remember the first issue of the newsletter when I said:

So, if you're debt-free and earning more than $3,000 a month, you're already doing well. If not, don't worry. You can reach that milestone—I believe in you!

It’s time to dive deeper into how you can crush your debts quickly, using two proven strategies: the Avalanche Method and the Snowball Method.

Avalanche Method

Pay off the debt with the highest interest rate.

After eliminating that debt, focus on the card with the next highest interest rate.

Repeat steps one and two until you are debt-free.

The Avalanche Method minimizes the overall amount of interest paid, which makes it the most cost-efficient in the long run.

It’s perfect for people who want to save as much as possible and are comfortable with delayed gratification since it might take longer to fully eliminate the first credit card’s balance.

Snowball Method

Pay off your smallest debt first, regardless of the interest rate.

Once that debt is eliminated, move to the next smallest one.

Repeat steps one and two until you are debt-free.

The Snowball Method gives you quick wins and builds momentum, thus helping you stay motivated.

It’s perfect for those who are overwhelmed and want to see progress fast.

You Don’t Really Own Your Investments

The reality of ownership in both stocks and cryptocurrencies is a bit of an illusion when it comes to traditional brokerage accounts. What most investors hold is not the actual asset, but rather an "IOU"—I Owe You—essentially a claim to the asset.

The term "IOU" comes into play because, in many cases, the brokerage holds the asset for you, but you don’t truly own it until certain steps are taken. For stocks, the shares you "own" are often held in what’s called "street name," which means they’re technically owned by the broker.

You have rights to them, yes, but they aren’t in your direct possession.

This also applies to crypto held on exchanges like Binance or Coinbase. While you see a balance in your account, the crypto isn’t technically in your control.

For stocks, you can mitigate this by opting for Direct Registration (DRS), which ensures that the shares are registered in your name with the company and are not held by a broker.

One of the biggest services providing DRS is Computershare, where you can register stocks like Apple, Tesla, and others. However, it's important to note that this method works for individual stocks—not for ETFs or mutual funds.

For cryptocurrencies, the solution is easier: move your crypto from the exchange to your own hardware or software wallet. By doing so, you regain control and ownership over your assets. The famous phrase is “Not your keys, not your coins,” and it holds true.

Life Hacks 2-Pack

Why Pay for Parking When a Fine is Cheaper

If you ever lose the parking pass from a mall or similar lot, it's often cheaper to pay the fine for the lost pass than to pay for your actual parking time. The same concept applies in other scenarios, too.

For example, parking in a prohibited area might cost you a $15 fine, while a nearby private lot charges $10 per hour.

On college campuses, you might be required to buy an expensive semester-long parking permit that runs into the hundreds of dollars. But parking without the permit may result in a small fine that, even if received a couple of times, is still much cheaper than the permit itself.

I'm not encouraging anyone to break the law—but it's something to think about.

You must also consider that some places have cameras that could catch you, some tickets more than once a day, or worse—your car could get towed, or penalties might add up.

One Bottle Can Slash Your Water Costs Forever

Have you ever found yourself suddenly thirsty, only to end up buying water at a café, restaurant, or grabbing a bottled water from a store? It's convenient, but it adds up over time.

Even though bottled water isn't that expensive, if you buy one bottle a day for an entire year, that could cost you anywhere from $100 to $365, depending on where you live. While $100 might not seem like much, small savings like this—$100 here, $100 there—can add up to $1,000 or more by the end of the year.

So what's the alternative?

Invest in a stainless steel water bottle. There are tons of versions and sizes available to fit your needs. It's better for the environment, better for your wallet, and better for your health, as you stay hydrated throughout the day.

Thank you so much for going through this week's insights. Hope you found them useful.

Catch you next Thursday!